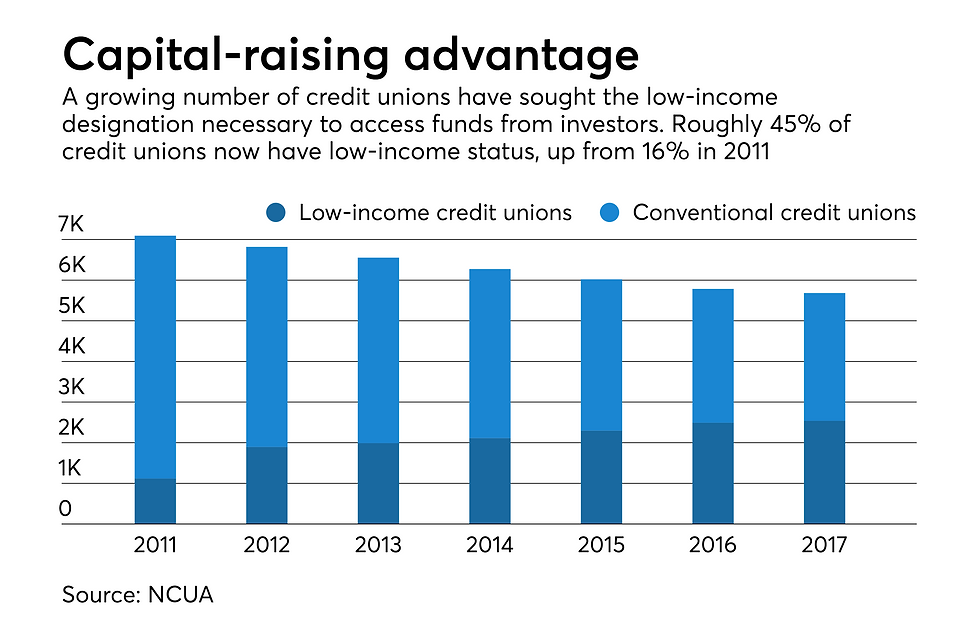

Another Low-Income CU Draws Record Secondary Capital Investment Credit Union JournalDec 20, 20173 min readUpdated: May 15, 2023A second credit union has announced plans to take on a record amount ofsecondary capital, a trend that is alarming bankers and drawing attention fromother credit unions.Notre Dame Federal Credit Union in Notre Dame, Ind. said late last week that itraised $12 million from a new fund created to provide secondary capital to creditunions. That followed a move by Jefferson Financial Federal Credit Union lastmonth, which disclosed plans to bring on an identical amount as part of a transaction credit union officials called the largest secondary capital raise in the industry’s history.The $530.2 million-asset Notre Dame, which has been growing loans significantlyfaster than banks and other credit unions, plans to use the new capital to drivefurther growth.“This injection of secondary capital...provides us the potential for immediategrowth that otherwise would have taken years to achieve,” Notre Dame CEOThomas Gryp said in a press release.Through the first nine months of 2017, Notre Dame grew its loan portfolio 12.35%to $450.2 million. Over the same span, loans industry-wide grew less than 8%;banks, by contrast, saw their loans grow just 2.7%.Gryp labeled secondary capital a potential “game-changer.” Dennis Dollar, aformer chairman of the National Credit Union Administration who now works as aprominent industry consultant, said that “there is no question there is a growingdemand for capital” among credit unions seeking to expand their branchnetworks,upgrade technology or venture into new lines of business.“I don’t think supplemental capital will ever be a way for a poorly capitalizedcredit union to build its net worth because the cost is just too high...but it couldbecome a viable option for a well-capitalized credit union that needs dollars forstrategic investment,” Dollar wrote Tuesday in an email to American Banker.Overall, the amount of secondary capital on credit unions’ books remainsrelatively small, totaling $150.6 million at the end of the third quarter, so it hasn’tbeen a hot-button topic for banks—but that may be changing.“It’s a trend we’ve been watching,” Brittany Kleinpaste, director of economicpolicy and research at American Bankers Association said in an interview.In a similar vein, James Kendrick, first vice president for accounting and capitalpolicy at the Independent Community Bankers of America, called secondarycapital use by credit unions “a troubling issue.”“It shows a theme that’s emerging with credit unions in general. They’re misusingthe purpose of the credit union charter and growing into these large, too-big-to-fail financial institutions,” Kendrick said. “Hopefully members of Congress willtake notice.”By law, only institutions that have been designated as low-income credit unionsby the industry’s regulator, the National Credit Union Administration, can issuesecondary capital. But the number of credit unions with the low-incomedesignation has been increasing steadily, even as the total number of creditunionshas declined. Through Sept. 30, a total of 2,538 credit unions weredesignated as low-income, up from 1,119 in 2011.“Now, we’re seeing these credit unions becoming comfortable and figuring outhow they can use that designation to their advantage,” Kleinpaste said.Michael Macchiarola, a partner at Olden Lane Advisors LLC, which created thenew Credit Union Secondary Capital Fund in partnership with Credit UnionCapital Management Services, an Overland Park, Kan.-based credit unionservice organization, said it was created solely to provide secondary capital tocredit unions.“We are pleased to be able to assist in their responsible growth and offer lendersan attractive return on a diversified pool of borrowers at the same time,”Macchiarola said in a press release last week.Neither Olden Lane nor Credit Union Capital Market Solutions responded to arequest for comment.Last month, working without Olden Lane, Credit Union Capital Market Solutionsarranged a deal that yielded$12 million in secondary capital for Metairie, La.-based Jefferson Financial.Both Notre Dame and Jefferson Financial acquired their capital in the absence ofa comprehensive regulation governing the use of alternative capital bymainstream credit unions. NCUA has been in the process of drafting such a planfor nearly a year, and Dollar urged them to finish the job.“To their credit, NCUA is actually approving some of those [applications],” hewrote. “They now need to enact a regulation putting some meat on the bones sothat eligible credit unions can know how to structure their supplemental capitalinitiatives and to make sure they are within a safe harbor of what NCUA willallow.”Kleinpaste and Kendrick had a different suggestion. Credit unions weighing theuse of secondary capital should explore becoming banks, instead.The ability to tap capital markets, expand member business lending authority andwiden fields of membership “all serve to make credit unions look more likebanks,” Kleinpaste said.By John ReostiDecember 20, 2017

CMCD 1st Issuance Press ReleaseJanuary 22, 2026 FOR IMMEDIATE RELEASE : Today, CU Capital Market Solutions is announcing the issuance of a new 3-year note. CREDIT UNION SHARE CERTIFICATES COLLATERALIZED NOTES PROGRAM CU Deposit Fun